Is Base "Stealing" Ethereum's GDP?

Ethereum urgently needs to shift its culture from "values alignment" to an enterprise-focused "Security-as-a-Service" business model.

Original Article Title: Is Base 'Stealing' Ethereum's GDP?

Original Article Author: Michael Nadeau, Founder of The DeFi Report

Original Article Translation: xiaozou, Jinse Finance

Standard Chartered Bank sparked a heated discussion last month with its report titled "Ethereum's Midlife Crisis." The report estimated that Base caused a $500 billion evaporation of Ethereum's market value and "took over GDP," thereby lowering the year-end price target for ETH from $10,000 to $4,000. This raises a fundamental question: Did Standard Chartered misjudge ETH at the L2 "J-curve" bottom, or will the structural decline continue?

In this article, we will re-examine Standard Chartered Bank's conclusions and offer our own insights.

1. Base's "Partnership" with Ethereum

Let's assume you are Ethereum, and I am Base. We are both building critical infrastructure for web3. One day, I propose to you: Instead of competing with L1, why not collaborate?

As Base, my partnership requirements are:

· Share Ethereum's security and settlement layer (self-built validators are too costly)

· Establish a native cross-chain bridge to Ethereum users and assets

· Share liquidity and developer ecosystem

· Reduce operating costs

· Be compatible with EVM and surrounding infrastructure

As Ethereum, you hope:

· Acquire new users through Coinbase channels

· Increase ETH demand (transactions and on-chain services)

· Receive feedback from enterprise customers

· Create fee revenue for validators

· Improve throughput and user experience

The synergy of 1+1>3 is formed between the two parties. Now, after two years, let's validate the results with on-chain data.

2. Base's Economy and On-Chain Data

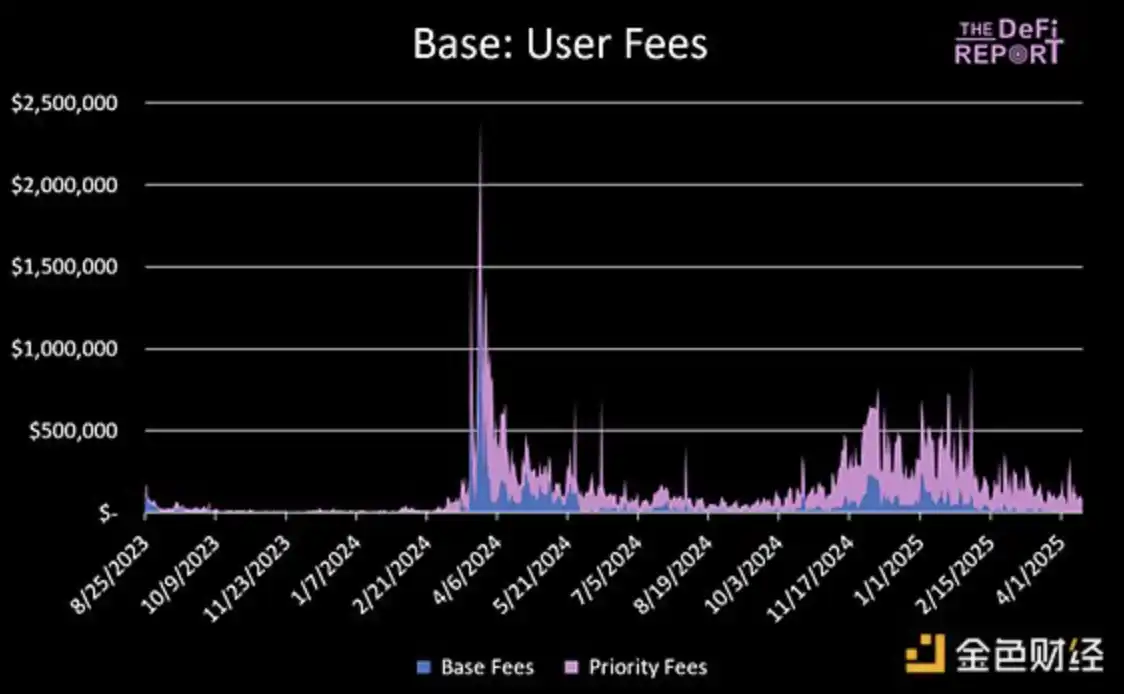

User Fees

Since its inception, Base has accumulated $24.8 million in base fees and $81.9 million in priority fees. In 2024, Base's revenue ($74 million) accounted for 1.1% of Coinbase's total annual revenue.

Base is currently the fastest-growing and most profitable Ethereum L2, launched two years after its main competitor Arbitrum.

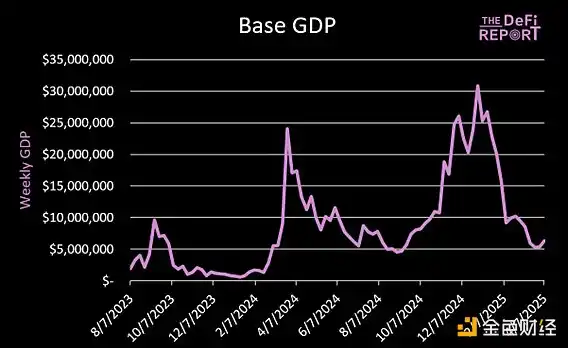

Base GDP

Base's on-chain applications have generated a total of $768 million in fees (cumulative "GDP"), with major contributors including DeFi protocols such as Uniswap and Aerodrome.

"GDP" measures the fees paid by end users to use on-chain applications (excluding gas fees).

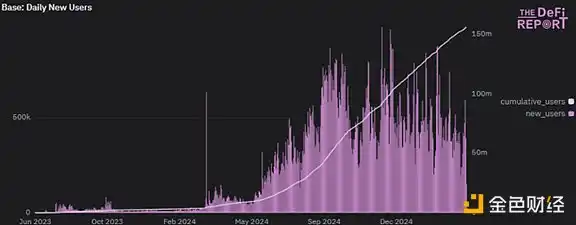

Daily New Addresses

Over the past 30 days, Base has averaged 412,000 new addresses per day. Since its launch in August 2023, Base has attracted a cumulative 155 million interacting addresses. Base is actively onboarding new users to the Ethereum ecosystem.

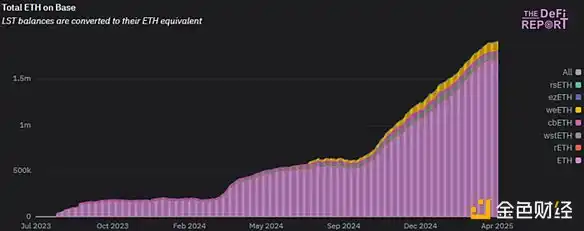

Base Bridged ETH

Currently, Base's layer has 1.917 million ETH (including LST), accounting for 1.6% of the circulating supply, creating new demand for ETH.

Daily Bridged Assets

Through native cross-chain bridges, $0.5-2 billion in assets flow between L1/L2 daily (ETH accounts for 80%). In the past 30 days, $5.03 billion in assets flowed back to Ethereum from Base. Over the last 90 days, $30 billion in assets flowed back to Ethereum from Base, confirming Ethereum's role as a cross-chain hub.

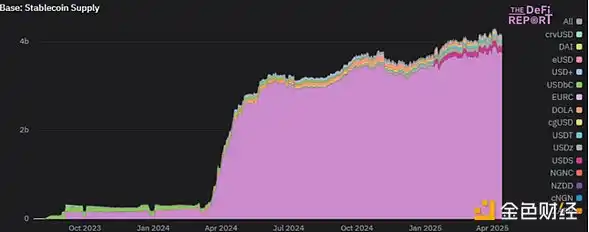

Stablecoin Supply

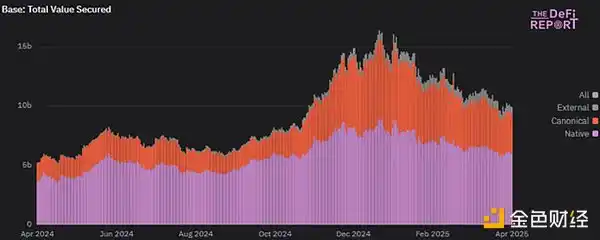

Base's on-chain stablecoin supply stands at $4.2 billion ($USDC accounts for 91%), with a total locked value of $9.9 billion, of which $6 billion is native assets and $3.3 billion are from Ethereum cross-chain. This has created more use cases for Ethereum.

Base is currently valued at 9.9 billion US dollars. Of this value, 6 billion US dollars are from "native" assets, meaning these assets were issued on Base. 3.3 billion US dollars are from "canonical" assets, indicating these assets were bridged from Ethereum. 0.6 billion US dollars are considered "external" assets, implying these assets were bridged from other chains.

Likewise, Base has created net new demand for ETH through native tokenized assets.

In summary, in less than two years, Base has leveraged Ethereum to:

• Become the largest and fastest-growing L2, earning 106 million US dollars in user fees.

• Introduce 157 million new addresses to Ethereum (including some L1 user migrations).

• Build an app ecosystem generating 768 million US dollars in fees.

• Bridge 1.91 million ETH cross-chain, creating additional on-chain service demand.

• Increase stablecoin value by 4 billion US dollars (Coinbase holds approximately 50% of USDC).

• Issue 6 billion US dollars of native assets while introducing 3.3 billion US dollars of Ethereum assets.

We believe Ethereum has achieved a collaborative value of 1+1=3 in this case. But how has Ethereum itself benefited?

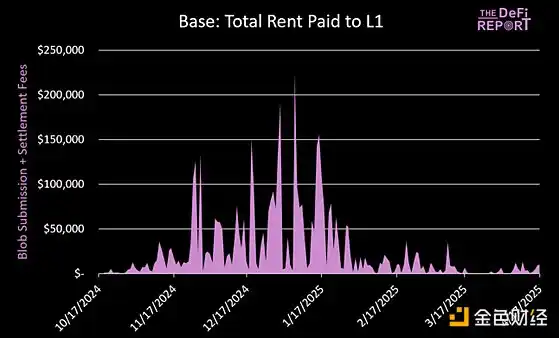

3. Base's Contribution to Ethereum's "Security Capture"

Base has cumulatively paid 4.5 million US dollars in L1 blob and settlement fees (which were burned), with an on-chain profit margin of 91% in the last six months (excluding off-chain costs). It is worth noting that Base has paid a total of 24 million US dollars in L1 fees, with 80% occurring before the EIP4844 implementation (cheaper blob), and our analysis does not include the earlier call data phase.

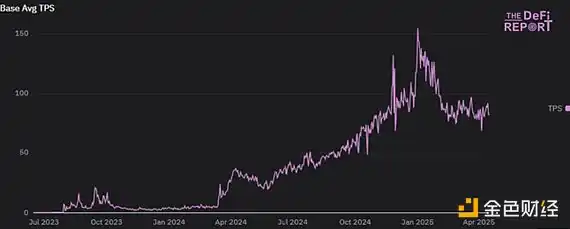

Currently, Base averages 93 TPS, effectively scaling Ethereum's capacity.

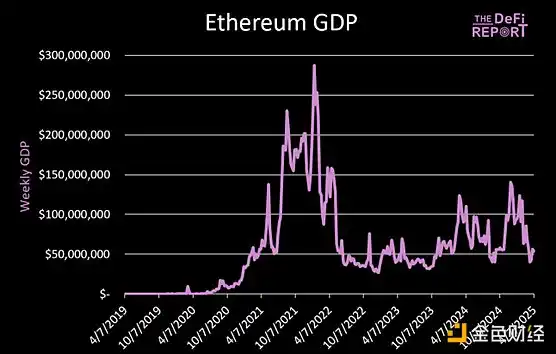

Since Base went live in August 2023, Ethereum's weekly GDP has grown by 75%, but is still 80% below the early 2022 peak. The current L1 app daily GDP is 57 million US dollars, while Base's weekly average app GDP reaches 6.8 million US dollars.

Back to the core question: Does Base "steal" Ethereum's GDP?

The answer is yes!

This is precisely the significance of the L2 roadmap. Top applications (such as Uniswap, Aave) are scaling on Base, while new projects (such as Aerodrome) are choosing Base directly over L1. User migration to L2 is causing a decrease in L1 fees and ETH burn, leading Ethereum to shift towards a more enterprise/B2B-oriented business model.

Only when L2 can't bridge the gap through blob fees in the future does this constitute an "issue" for Ethereum.

4. Base Growth Projection and ETH Value Capture

Based on current data, we believe Ethereum is investing in a long-term future through the L2 roadmap, sacrificing short-term GDP, fees, and ETH burn, with the hope that Base can scale, establish a replicable template (traditional finance?), and drive positive ecosystem development.

Current Situation Analysis:

• L2 currently processes approximately 165 TPS in total, needing to compete for blob space.

• 3-4 L2s consistently fill the current target of 3 blobs per block (maximum of 6), whenever this happens, L2s compete, driving fees up.

• The target blobs/block is currently 3 (maximum of 6), but next month, an upgrade through Pectra will increase it to 6 (maximum of 9 blobs/block). Hence, in the initial scenario analysis, we assume a target of 6 blobs, with a maximum of 9 blobs.

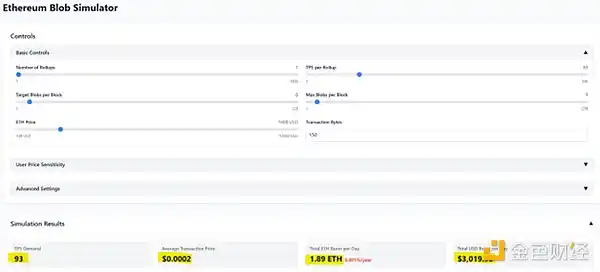

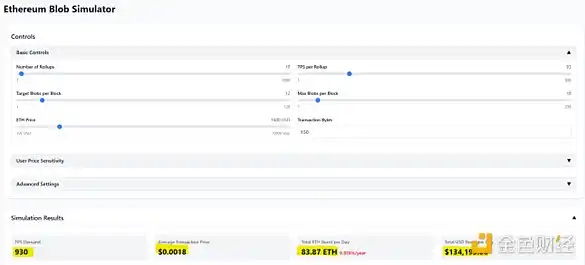

• We are using the Blob Simulator created by Tim Robinson.

As seen in the above diagram, the current state has minimal impact on the Ethereum economy, with L2 averaging a fee of $0.0002.

A 5x increase in Base TPS would result in slightly higher L2 fees, while bringing more value to Ethereum L1 (annualized $24.5 million).

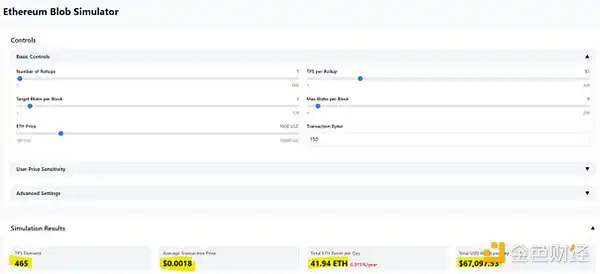

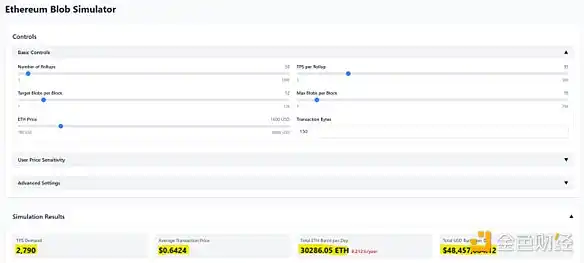

Increasing Base TPS by 10x would result in a 200x surge in L1 annual revenue to $4.9 billion (welcomed by validators). However, we have also created another issue: L2 average fee will rise to $0.35 (unacceptable).

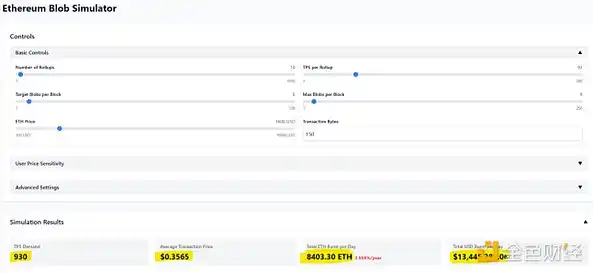

The PeerDAS and Fusaka upgrades (expected in Q3/Q4 this year) will increase the blob reward per block to 12 (ultimate goal of 48, maximum cap of 72). Assuming a 10x increase in Base TPS and completion of the initial Fusaka upgrade:

• L2 average fee can be kept at $0.0018

• L1 annual revenue $48.9 million

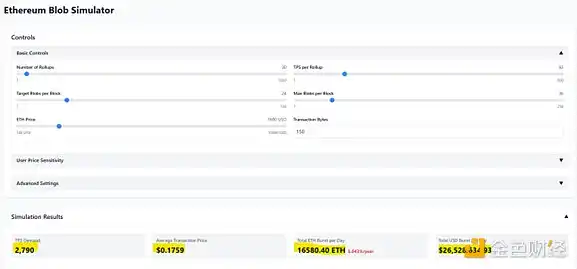

If Arbitrum and Optimism also achieve a simultaneous 10x expansion:

• L1 annual revenue could reach $17.7 billion (nearly double the 2021 peak)

• But once again, we have created a bottleneck, with average L2 cost per transaction rising to $0.64. This is not feasible.

Let's optimistically estimate that the target blob will increase to 24 in a year:

• L1 annual revenue will decrease to $9.6 billion

• L2 average fee remains at $0.17

To keep the L2 average fee below $0.02, we need 33 target blobs per block, at which point L1 annual revenue is only $1.4 billion—just matching the actual revenue from the past 365 days.

Summary:

We have tried to simplify the analysis model, aiming to clarify two core mechanisms: 1) The impact of L2 transactions per second (TPS) increase on blob pricing; 2) The transmission effect of an increased L1 target blob/block quantity on the Ethereum economic model and L2 user fees. In reality, we fully understand the dynamics and unpredictability of the market environment—there may be hundreds of L2s vying for blob space in the near future.

We are confident that L1 will still host a significant amount of on-chain activity, continue to generate fee revenue, and drive ETH burning. However, specific use cases and transaction scales are currently unclear.

Based on simulation results (assuming the three major L2s each reach a 10x TPS increase from the current Base), when the total L2 TPS reaches 2,790, even with the completion of the Pectra technology upgrade, the Ethereum network will still face overload pressure (at this point, L2 single transaction cost reaches $0.35).

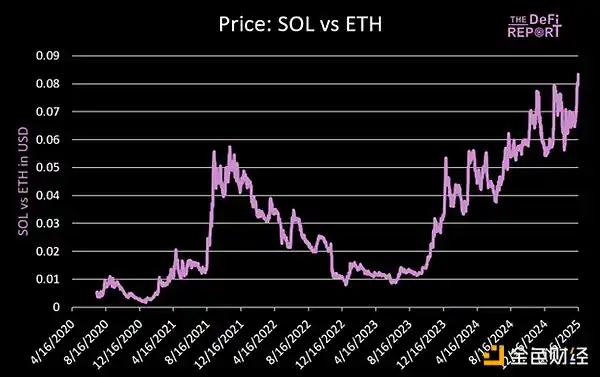

In contrast, Solana has consistently processed 1,078 TPS over the past 90 days, with an average fee of only $0.016 (including base fee + priority fee), and the actual user fee is even lower—due to its network's dynamically priced transaction mechanism by transaction type, and its performance upgrade plan Firedancer has not yet been officially launched.

5. Conclusion

The saying "There is no perfect solution, only trade-offs" is particularly relevant here. Base quickly gained momentum through the L2 model, currently achieving ideal returns, but has also tied itself to the uncontrollable Ethereum scaling path, potentially facing "vendor lock-in" and technical debt risks.

Ethereum seems to have sacrificed L1 fees to attract enterprise clients, create ETH demand, and improve user experience. However, the sustainability of long-term economic relationships is questionable—scenario analysis shows that scalability bottlenecks may persist. If L2 cannot scale quickly, it may be necessary to issue more ETH to maintain validator rewards (after EIP4844, the ETH supply has changed from deflationary to potentially exceeding BTC).

We believe that Base is satisfied with the current situation, but if Ethereum's blob scaling is not effective, it may seek alternative solutions such as Celestia. Ethereum urgently needs to shift its culture from "values and identity" to an enterprise-oriented "security-as-a-service" business model.

Returning to the original question: Has Standard Chartered Bank misjudged the "L2 J-curve" bottom? We believe that the fundamental structural decline of Ethereum will continue in the short term. Although the onboarding of traditional finance may improve market sentiment, there is a lack of fundamental improvement catalysts. The following chart shows that there is still a long way to go.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Trump admits his statement of "ending the Russia-Ukraine conflict within 24 hours" was a joke

Data: BlackRock and six other entities account for 88% of tokenized treasury issuance

Top 5 Altcoins Between $100M–$1B with 5x Growth Potential in 2025

Bitcoin Bounce Triggers Rally: 4 Real World Asset Tokens Gain Over 80%